The decision to take no further action on the complaints against Temer has virtually started the election campaign for the presidential elections of October 2018.

The polls for a moment look at a ballot between Lula and Bolsonaro, but the journey is still very long and hardly this “odd couple” will have the strength to come to the final end (also because on Lula is weighing the sentence to nine and a half years of prison imposed by Judge Sergio Moro).

Among the most recent novelties in the presidential race, appeared the candidature – still unofficial – of João Dionisio Amoêdo, the Partido Novo founder (https://novo.org.br/). Amoêdo is an engineer, business manager and, most recently, a partner of the BBA bank.

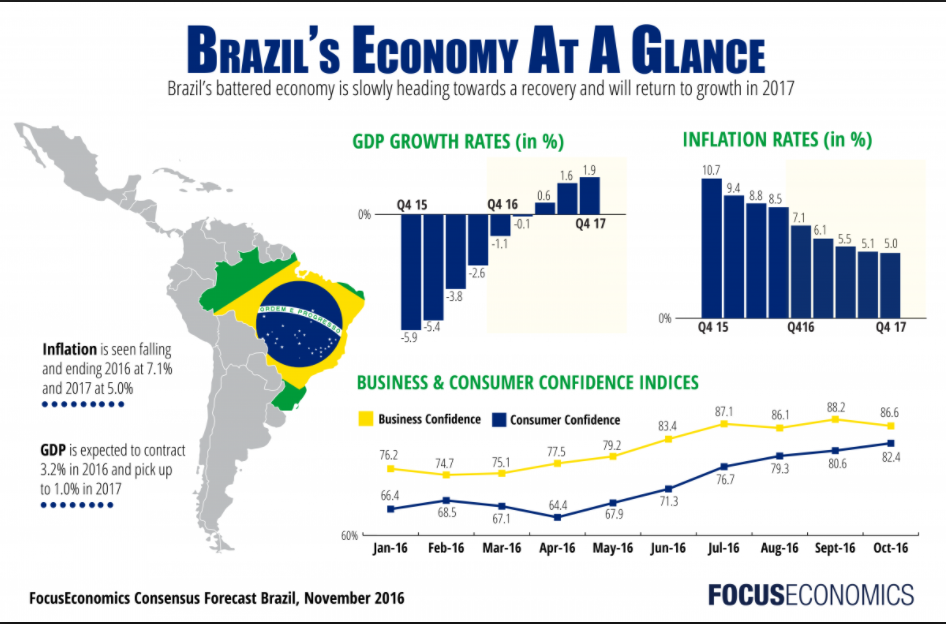

On the economic front, on 25/10/2017 at the Copom meeting, Banco Central decided to further decrease the discount rate (SELIC), bringing it to 7.5% per annum. This is the lowest value in 4 years.

The growth of public debt continues, in September reached 73.9% of GDP. This is a relatively modest level when compared with the debt of other western countries, but growing strongly due to the continuing imbalance in public accounts (mainly due to the social security deficit).

The auction for oil exploration “pre-sal” was successful. The National Petroleum Agency (ANP) estimates royalties revenue ranging from US$ 120 to US$ 180 billion between 2022 (start date of oil production) and 2054.

Let’s see some updated data:

GDP (Value added at market prices)

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| GDP – real growth (%) | 1,8% | 2,7% | 0,1% | -3,9% | -3,6% | 0,73% | 2,50% |

Growth forecasts for GDP growth 2017 are stable; slightly increased for 2018.

The market had already taken over the political crisis linked to the denunciations against Temer and this month no new signs of accelerating economic growth emerged.

Inflation and real/dollar exchange

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| IPCA (IBGE – %) | 5,80% | 5,90% | 6,40% | 10,67% | 6,29% | 3,08% | 4,02% |

The inflation forecast 2017 is slightly up, back above the minimum threshold (3%) scheduled for 2017 by the Brazilian Banco Central. Stable forecasts for 2018, around 4%.

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Exchange rate R$/US$ (end of the period) | 2,04 | 2,34 | 2,66 | 3,90 | 3,25 | 3,19 | 3,30 |

Real / dollar exchange rate forecasts have increased. in recent days the exchange rate has marked rather substantial fluctuations. The year-end change is expected at R $ 3.19, although today the dollar is quoted at 3.27, against 3.17 a month ago.

The dollar is thus recovering thanks to the good performance of the US economy, the signs of continuity in the Fed’s government and the prolongation of the “quantitative easing” announced by the ECB.

The euro is now around 3.81 reais, up from 3.73 in the beginning of October.

Interest rate

| 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

| Nominal Interest rate (end of the períod) | 7,30% | 10,00% | 11,80% | 14,87% | 13,75% | 7,00% | 7,00% |

| Real interest (deflactor: IPCA) | 2,50% | 2,10% | 4,20% | 2,60% | 6,91% | 3,92% | 2,98% |

The forecasts for the discount rate (SELIC) at the end of 2017 and 2018 remained unchanged at 7%. In the last 2017 session (December 5th), Copom should reduce Selic’s other 0.5%, closing down the rebound cycle that began in 2016.

With inflation under control and economic growth in progress, for 2018 the market does not foresee further downturns.

The Brazilian stock market (Bovespa)

Still a fluctuating month for the Brazilian stock market, which still stands close to the historic 76,000 points. Today Ibovespa is around 74,300 points.

The next post, scheduled for 20/11/2017, will look more closely at Bovespa’s performance over the past 12 months.

Article written by Mauro Mantica and published on “Update Brazil”. Available here.